The sharp rise in raw material prices deeply impacts the European agricultural machinery industry

***

Brussels, 16/06/2021

Since March of this year, inflation has risen sharply in all industrialized countries, particularly in the United States, where it reached 4.24% in April, the highest annual trend since 2008. One has to go back to the early 1990s to see inflation reach such a level. While the general rise in prices in Europe has not yet reached this pace, there is a clearly identified risk, according to Eurostat's statistical series, that inflation will accelerate in the coming weeks, due to the sharp rise in commodity prices that has recently been observed. For instance, energy prices have risen by 13%, on an annualized basis, over a single month.

Inevitably, higher energy prices will be reflected in production costs and consumer prices. Unfortunately, for our industry, the rise in raw material prices does not only concern energy. It affects all the raw materials that are essential for producing agricultural equipment.

This is particularly true of the price of steel, which has more than doubled in one year, from 550 euros per ton to 1,250 euros per ton. In our industry, steel, depending on the type of equipment, represents 30 to 40% of the average production cost. The prices of all products derived from petroleum chemistry are also rising. This is the case for ST plastic, used by our industry, whose prices have risen by 70% in six months.

Non-ferrous metals such as aluminium and copper are also greatly affected by this general price increase. Since April 2020, the price of aluminium has increased by 50%.

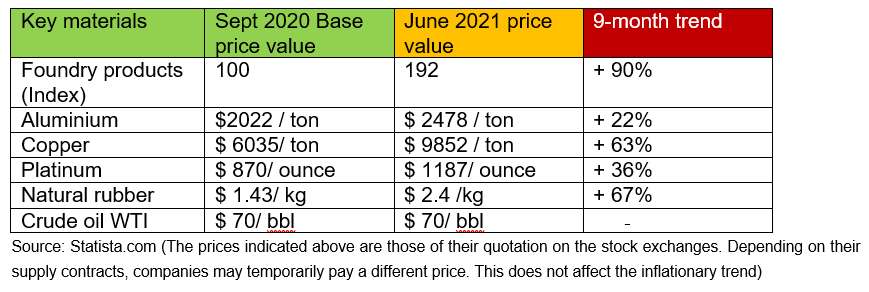

The table below illustrates the price variations of the main raw materials used by our industry in its manufacturing processes, between September 2020 and June 2021.

This table shows a clear upward inflationary trend for all key materials over these last 9 months, noticeably for foundry products (+90%), Copper (+63%) and natural rubber (+36%). To this picture, we should add the deep crisis in electronic components that has affected all industries since March. Although production has returned to pre-pandemic levels, a surge in demand for electric vehicles, household appliances and cell phones has created a supply shortage, resulting in increased costs throughout the value chain and, in some cases, production delays.

Furthermore, global logistic is highly disrupted by the unexpected recovery. There is also a shortage of ships and containers being available. The prices per container tripled these last months from $2,500 to $7,500. This also leads to additional costs and delays to import parts and accessories from Asia to Europe.

CEMA members are particularly concerned about this strong inflationary surge, which, even if it were temporary, is affecting them at a time when their plants traditionally reach a production peak. This is an unfortunate combination of the seasonality of our industry and the inflationary surge.

In this worrying context, CEMA hopes that the lifting of all trade restrictive measures on steel and aluminium imports into the European Union, announced for the end of June, will limit the rise in steel prices for both producers and consumers. CEMA will remain particularly attentive to the evolution of inflation, because if it were to become structural, it would pose a lasting threat to the current recovery.

CEMA members will be kept informed as the economic environment evolves and hopefully normalizes by next fall.